Summary

Recently a leading Non-Banking Financial Company (NBFC) in India faced significant challenges in expanding its lending operations to underserved segments while maintaining acceptable risk levels. The solution leveraged alternative data sources, particularly device parameters and personal data, to create a more inclusive credit scoring system that could accurately assess creditworthiness beyond traditional metrics.

We have implemented a comprehensive solution that included custom machine learning models, a secure data collection framework, and seamless integration with existing banking infrastructure. The system analyzed over 400 alternative data points from smartphone metadata, including app usage patterns, SMS logs, call records, and geolocation data, to generate accurate credit risk profiles.

The results were remarkable; loan approval rates increased by 28%, default rates decreased by 32%. Most importantly, the solution enabled the client to extend credit to previously underserved segments, including young borrowers, rural customers, and those with limited credit history, contributing significantly to financial inclusion in India.

Introduction to the Indian Lending Landscape

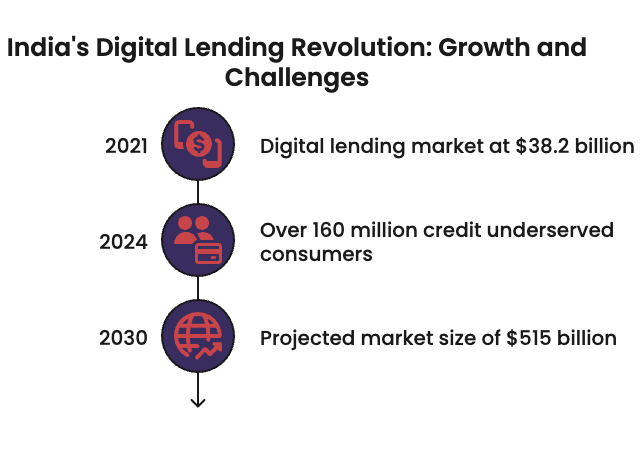

India’s digital lending ecosystem has experienced explosive growth in recent years, with the market projected to reach $515 billion by 2030, representing a 33.5% CAGR from $38.2 billion in 2021. This rapid expansion is driven by several factors, including increased smartphone penetration, growing digital literacy, and a significant unmet demand for credit among underserved segments.

The Indian lending sector has undergone a transformation, particularly in the post-pandemic era, with digital lending becoming a key driver of financial inclusion. The sector is characterized by a diverse range of players, including traditional banks, NBFCs, and fintech companies, all competing to capture market share in this rapidly evolving landscape.

Despite this growth, significant challenges persist. Traditional credit assessment methods rely heavily on credit bureau information, which covers only a fraction of India’s population. As of 2024, over 160 million consumers in India were considered credit underserved, with limited or no credit history. This creates a substantial barrier to financial inclusion, particularly for young borrowers, rural populations, and those in the informal economy.

The regulatory environment has also evolved significantly, with the Reserve Bank of India (RBI) implementing comprehensive guidelines for digital lending to address concerns related to data privacy, consumer protection, and responsible lending practices. These regulations have shaped how fintech companies approach credit assessment and lending operations, emphasizing the need for transparent, secure, and compliant solutions.

Client Background and Challenges

Our client, a mid-sized NBFC with a decade-long presence in India’s consumer lending market, had established a solid reputation for providing personal loans and small business financing through traditional channels. However, the company faced several critical challenges that limited its growth potential and ability to serve broader market segments.

Key Challenges:

-

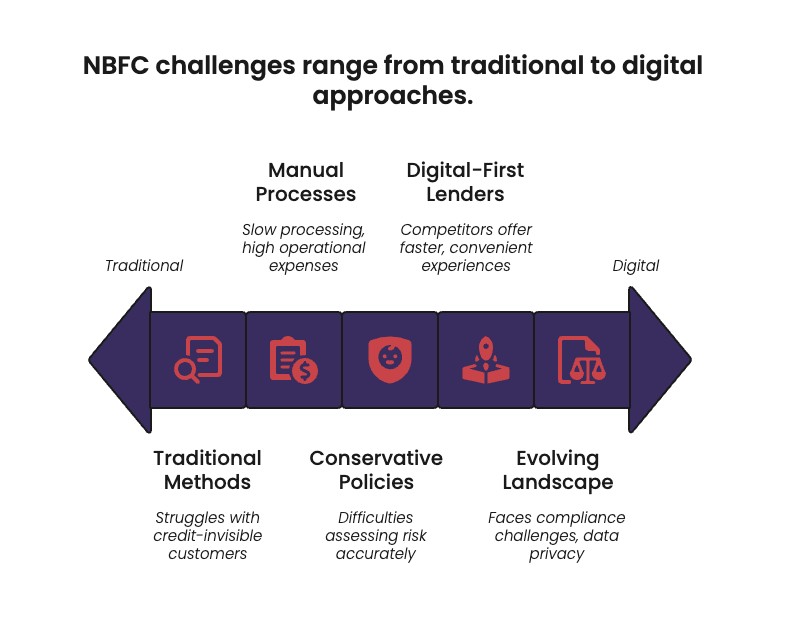

- Limited Market Reach: The client’s reliance on traditional credit assessment methods restricted their ability to serve the vast segment of credit-invisible customers, including young professionals, rural entrepreneurs, and gig economy workers.

- High Operational Costs: Manual verification processes and physical documentation requirements resulted in lengthy loan processing times (averaging 3-5 days) and high operational costs, making small-ticket loans economically unfeasible.

- Risk Management Concerns: Without reliable data on credit-invisible customers, the client faced difficulties in accurately assessing risk, leading to conservative lending policies and missed opportunities.

- Competitive Pressure: The rapid rise of digital-first lenders threatened the client’s market position, as these competitors leveraged technology to offer faster, more convenient lending experiences.

- Regulatory Compliance: Navigating the evolving regulatory landscape for digital lending in India presented significant compliance challenges, particularly regarding data privacy and consumer protection.

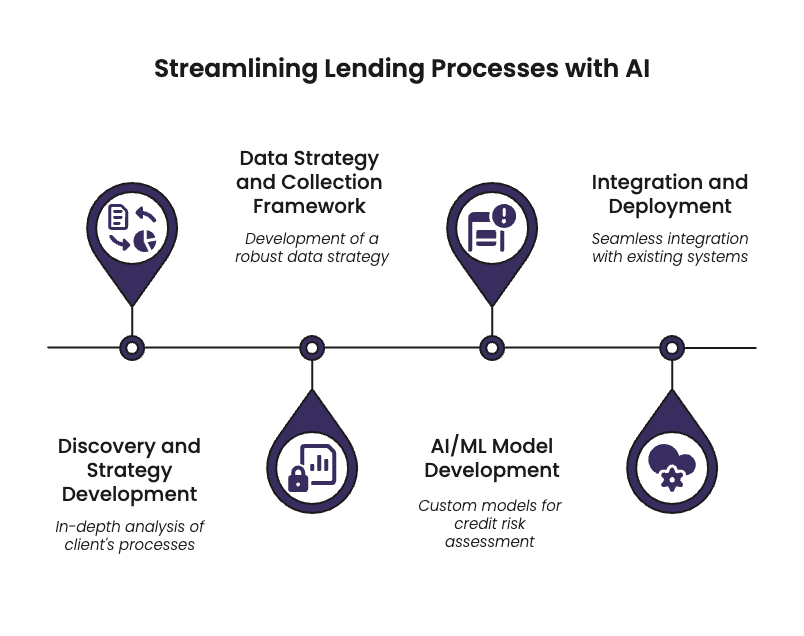

Phase 1: Discovery and Strategy Development

We began with an in-depth analysis of the client’s existing lending processes, technology infrastructure, and business objectives. This included:

-

- Conducting stakeholder interviews across departments to understand pain points and requirements

- Analyzing historical loan data to identify patterns and opportunities for improvement

- Benchmarking against industry best practices in digital lending

- Mapping regulatory requirements to ensure compliance by design

Based on this analysis, we developed a strategic roadmap that outlined the technical architecture, data sources, model development approach, and implementation timeline.

Phase 2: Data Strategy and Collection Framework

A critical component of our solution was the development of a robust data strategy that identified alternative data sources with high predictive power for credit risk assessment. We designed a secure, consent-based framework for collecting and processing device data and personal information, ensuring full compliance with Indian data privacy regulations.

The data collection framework included:

-

- A lightweight SDK that could be embedded in the client’s existing mobile application

- Clear consent mechanisms that explained data usage to borrowers in simple language

- Secure data transmission protocols with end-to-end encryption

- Data minimization principles to collect only relevant information

Phase 3: AI/ML Model Development

Leveraging our expertise in machine learning for credit risk assessment, we developed custom models that could analyze alternative data sources to predict creditworthiness. Our approach combined traditional statistical methods with advanced machine learning techniques to create a multi-layered scoring system.

Phase 4: Integration and Deployment

The final phase involved integrating our solution with the client’s existing loan origination system and core banking infrastructure. We implemented a microservices architecture that enabled seamless data flow between systems while maintaining security and scalability.

The deployment process included:

-

- Comprehensive testing to ensure system reliability and accuracy

- Staff training programs to familiarize employees with the new system

- Phased rollout strategy to minimize business disruption

- Continuous monitoring and feedback mechanisms for ongoing improvement

This methodical approach ensured that the solution addressed all of the client’s requirements while minimizing implementation risks and ensuring regulatory compliance.

Technical Implementation Details

System implementation involved several interconnected components designed to work together seamlessly. The architecture was built with scalability, security, and compliance as foundational principles.

System Architecture

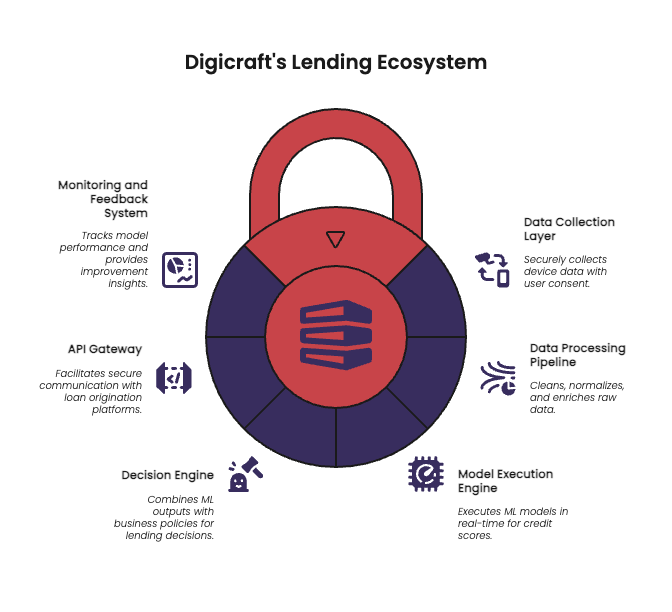

We implemented a cloud-native, microservices-based architecture that enabled modular development and deployment. The system comprised several key components:

- Data Collection Layer: A lightweight SDK embedded in the client’s mobile application that securely collected device data with explicit user consent.

- Data Processing Pipeline: A robust ETL (Extract, Transform, Load) pipeline that cleaned, normalized, and enriched raw data for model consumption.

- Model Execution Engine: A high-performance computing environment that executed the ML models in real-time to generate credit scores.

- Decision Engine: A rules-based system that combined ML model outputs with business policies to make final lending decisions.

- API Gateway: A secure interface that facilitated communication between our system and the client’s existing loan origination platform.

- Monitoring and Feedback System: A comprehensive dashboard that tracked model performance and provided insights for continuous improvement.

Data Security and Privacy Measures

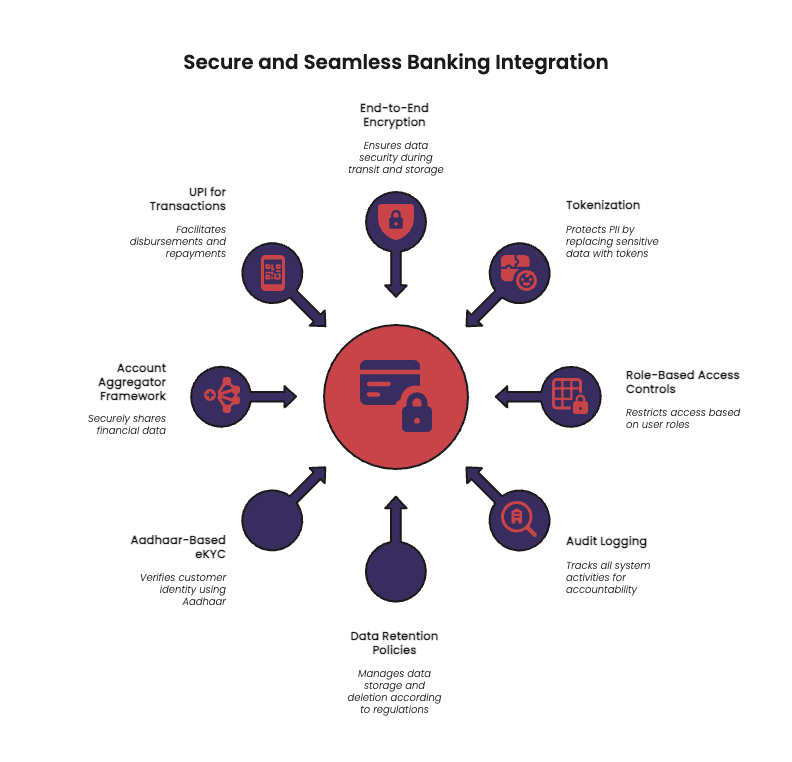

Given the sensitive nature of the data being processed, we implemented robust security measures throughout the system:

-

- End-to-end encryption for all data in transit and at rest

- Tokenization of personally identifiable information (PII)

- Role-based access controls with multi-factor authentication

- Comprehensive audit logging for all system activities

- Automated data retention and purging policies in compliance with regulations

Integration with Banking Infrastructure

A critical aspect of the implementation was seamless integration with the client’s existing banking infrastructure. We leveraged India Stack components, including:

-

- Aadhaar-based eKYC for customer verification

- Account Aggregator framework for secure financial data sharing

- UPI for disbursements and repayments

This integration enabled a frictionless experience for both the client’s operations team and end customers, while maintaining the highest standards of security and compliance.

AI/ML Models for Credit Scoring

The heart of our solution was a sophisticated ensemble of machine learning models designed to assess creditworthiness using alternative data sources. Rather than relying on a single model, we developed a multi-layered approach that combined the strengths of different algorithms to achieve optimal predictive power.

Model Architecture

Our credit scoring system comprised three primary model layers:

- Base Risk Assessment Models: These models analyzed traditional credit data (where available) along with basic demographic and application information to establish a foundational risk score.

- Alternative Data Models: Specialized models that extracted insights from device data, transaction patterns, and behavioral indicators to generate supplementary risk scores.

- Ensemble Meta-Model: A sophisticated model that combined outputs from the base and alternative data models to produce a final credit score, optimizing for both accuracy and explainability.

This layered approach allowed the system to make accurate predictions even when certain data points were missing, making it particularly effective for assessing thin-file or no-file borrowers.

Model Development Process

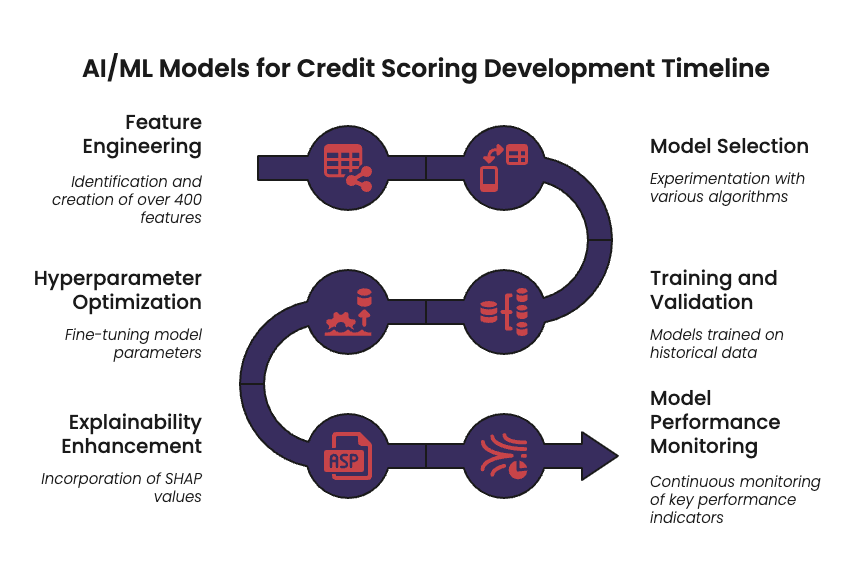

The development of our ML models followed a rigorous, iterative process:

-

- Feature Engineering: We identified and created over 400 features from raw data sources, including temporal patterns, frequency metrics, and derived indicators.

- Model Selection: We experimented with various algorithms, including logistic regression, random forests, gradient boosting machines, and deep neural networks, to identify the most effective approaches for different data types.

- Training and Validation: Models were trained on historical data with known outcomes, using cross-validation techniques to ensure robustness.

- Hyperparameter Optimization: We employed automated techniques to fine-tune model parameters for optimal performance.

- Explainability Enhancement: We incorporated explainability techniques such as SHAP (SHapley Additive exPlanations) values to make model decisions interpretable for both regulators and business users.

Model Performance Monitoring

To ensure ongoing effectiveness, we implemented a comprehensive model monitoring system that tracked key performance indicators:

-

- Predictive accuracy metrics (AUC, Gini coefficient)

- Population stability indices to detect data drift

- Feature importance stability to identify changing patterns

- Model calibration metrics to ensure probability estimates remained accurate

This monitoring system enabled continuous improvement of the models through regular retraining and refinement based on new data and changing market conditions.

Device and Personal Parameters Used

A key innovation in our solution was the extensive use of device parameters and personal data to assess creditworthiness. These alternative data sources provided valuable insights into borrower behavior and financial responsibility, particularly for individuals with limited credit history.

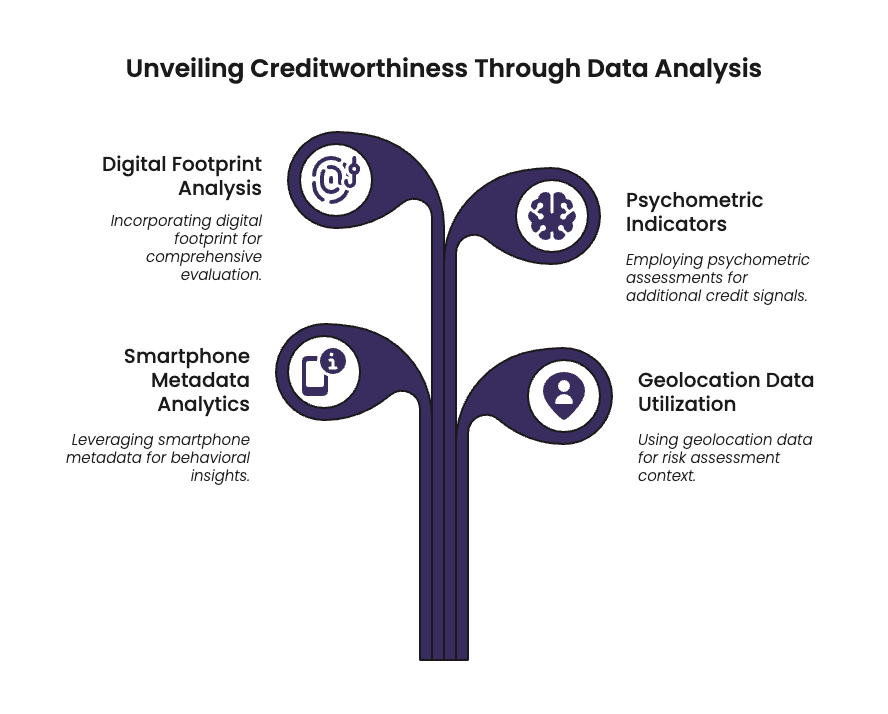

Smartphone Metadata Analytics

We leveraged various types of smartphone metadata, collected with explicit user consent, to build comprehensive behavioral profiles:

- App Usage Patterns: The types of apps installed, frequency of usage, and usage duration provided insights into financial behavior, lifestyle, and stability.

- SMS Logs Analysis: We analyzed financial SMS messages (such as salary credits, bill payments, and transaction alerts) to understand income patterns and financial discipline.

- Call Records: Call frequency, duration, and network stability served as proxies for social stability and reliability.

- Device Stability: Metrics such as device age, operating system updates, and storage management indicated responsibility and organization.

Geolocation Data Utilization

Geolocation data, when provided with consent, offered valuable context for risk assessment:

- Home and work location stability over time

- Travel patterns and consistency

- Correlation between declared address and actual location patterns

Digital Footprint Analysis

Beyond device data, we incorporated broader digital footprint elements:

- Email usage patterns and account age

- Digital transaction history (when available through account aggregation)

- Online behavior consistency

Psychometric Indicators

For certain customer segments, we incorporated optional psychometric assessments that measured traits like financial responsibility, honesty, and risk tolerance. These assessments provided additional signals, particularly for borrowers with very limited alternative data.

All data collection was conducted with strict adherence to privacy principles, including explicit consent, purpose limitation, data minimization, and secure processing. Users were provided with clear explanations of what data was being collected and how it would be used, with the option to decline without being excluded from traditional assessment methods.

Results and Impact

The implemented AI-driven lending ecosystem delivered significant measurable results for the client across multiple dimensions. These outcomes not only improved business metrics but also advanced financial inclusion objectives.

Operational Improvements

The solution dramatically transformed the client’s lending operations:

- Processing Time Reduction: Loan application processing time decreased from an average of 3-5 days to just 20 minutes, with some straightforward cases approved in as little as 5 minutes.

- Operational Cost Savings: The automation of credit assessment and verification processes reduced operational costs by approximately 42%, enabling the client to profitably serve smaller ticket loans.

- Scalability Enhancement: The digital-first approach allowed the client to scale their lending operations by 3.5x within 12 months without proportional increases in operational staff.

Credit Performance Metrics

The AI/ML models demonstrated superior predictive power compared to traditional credit assessment methods:

- Approval Rate Increase: Loan approval rates increased by 28% while maintaining the same risk appetite, primarily by identifying creditworthy borrowers who would have been rejected by traditional methods.

- Default Rate Reduction: Despite the expanded borrower base, default rates decreased by 32% compared to the previous assessment system, demonstrating the superior risk discrimination of the ML models.

- Risk-Adjusted Return Improvement: The combination of higher approval rates and lower defaults resulted in a 45% improvement in risk-adjusted return on assets for the client’s personal loan portfolio.

Financial Inclusion Impact

Perhaps most significantly, the solution enabled the client to extend credit to previously underserved segments:

- Young Borrowers: 61% of approved borrowers were under the age of 30, many accessing formal credit for the first time.

- Rural Penetration: 24% of loans were disbursed to borrowers in rural areas, compared to just 8% before implementation.

- Thin-File Customers: Approximately 35% of approved borrowers had limited or no credit history in traditional bureau reports.

- Small Ticket Loans: The average loan size decreased by 18%, indicating greater accessibility for borrowers with smaller credit needs.

Customer Experience Enhancement

The solution also delivered significant improvements in customer experience:

- Application Simplification: The number of fields in the loan application form was reduced by 60%, while the predictive power of the assessment increased.

- Faster Disbursements: Funds were typically disbursed within 2 hours of approval, compared to 1-2 days previously.

- Reduced Documentation: For many borrowers, the need for physical documentation was eliminated entirely, with verification conducted through digital channels.

These results validated the effectiveness of alternative data-driven credit assessment and demonstrated the potential of AI/ML technologies to transform lending operations while advancing financial inclusion objectives.

Regulatory Compliance Considerations

Navigating India’s evolving regulatory landscape for digital lending was a critical aspect of our solution design and implementation. We ensured that all aspects of the lending ecosystem complied with relevant regulations while anticipating future regulatory developments.

Adherence to RBI Digital Lending Guidelines

The Reserve Bank of India (RBI) has issued comprehensive guidelines for digital lending to address concerns related to transparency, data privacy, and consumer protection. Our solution incorporated these requirements by design:

- Direct Disbursement: All loan disbursements and repayments were executed directly between borrowers and the client’s bank accounts, as mandated by RBI guidelines.

- Transparency in Lending: The system provided clear, upfront disclosure of all loan terms, including interest rates, fees, and annual percentage rates (APR).

- Consent-Based Data Usage: Explicit, purpose-specific consent was obtained for all data collection, with clear explanations of how data would be used.

- Grievance Redressal: A robust mechanism for addressing customer complaints was integrated into the platform, with defined escalation paths and resolution timeframes.

Data Privacy and Protection

With the implementation of the Digital Personal Data Protection Act in India, data privacy considerations were paramount in our solution design:

- Data Minimization: We collected only the data necessary for credit assessment, avoiding excessive data gathering.

- Purpose Limitation: All collected data was used solely for the stated purpose of credit assessment and fraud prevention.

- Storage Limitation: Clear data retention policies were implemented, with personal data purged after its purpose was fulfilled.

- Security Safeguards: Comprehensive technical and organizational measures were implemented to protect data from unauthorized access or breaches.

Responsible AI Practices

Beyond regulatory requirements, we implemented responsible AI practices to ensure fairness and transparency in credit decisions:

- Algorithmic Fairness: Models were tested for bias across demographic groups, with adjustments made to ensure equitable outcomes.

- Explainability: The system provided clear explanations for credit decisions, helping borrowers understand the factors that influenced their assessment.

- Human Oversight: While automation streamlined the process, human review was incorporated for edge cases and appeals.

- Regular Audits: The system underwent regular audits to ensure continued compliance with evolving regulations and ethical standards.

By prioritizing regulatory compliance and ethical considerations from the outset, we created a solution that not only met current requirements but was also adaptable to future regulatory developments.

Conclusion

The results speak for themselves: a 28% increase in approval rates, a 32% reduction in defaults, and dramatic improvements in processing speed and operational costs. Most importantly, the solution extended credit access to young borrowers, rural populations, and thin-file customers who had been excluded by traditional assessment methods.

This implementation highlights several key lessons for financial institutions seeking to innovate in India’s dynamic lending landscape:

-

- Alternative Data Value: Device parameters and digital footprints contain powerful signals about creditworthiness that can complement or replace traditional credit information.

- Regulatory-First Design: Building compliance into the solution architecture from the outset is essential for sustainable innovation in regulated financial services.

- Balanced Automation: While AI can dramatically improve efficiency, maintaining appropriate human oversight ensures fairness and builds trust.

- Continuous Evolution: The lending ecosystem must continuously adapt to changing market conditions, customer needs, and regulatory requirements.

As India’s digital lending market continues its rapid growth trajectory toward $515 billion by 2030, solutions that effectively balance innovation, inclusion, and compliance will be essential. The future of lending in India will be increasingly data-driven, with alternative sources providing the key to unlocking credit access for millions of previously excluded individuals and businesses. By embracing these innovations responsibly, financial institutions can play a pivotal role in India’s journey toward comprehensive financial inclusion and economic empowerment

Reach Out to Us

At DigiCraft Technovision Private Limited, we are passionate about leveraging AI/ML technologies to solve real-world problems in Fintech space and beyond. If you have any questions about this project or want to explore how AI can transform your business operations, feel free to reach out!

Email us at [email protected]

Visit our website at https://digicraft.ai

Let’s collaborate and innovate together!